Basel 4 en Basel 3.5 explained.

Basel 4 sets far-reaching new rules for the weighting of credit risks (and operational and market risks). This weighting is important for the way in which banks calculate their capital ratios ('buffers').

Higlights Basel Framework

Capital positions and requirements comparable

The Basel 4 proposals are intended to make the capital positions and capital requirements of banks more comparable internationally: how much capital do banks have as a 'buffer' and does that amount of capital match the risks of their exposures?

The 2017 Basel 4 proposals are seen as the finalization of Basel 3

The international supervisory framework that consists of a package of measures taken after the credit crisis in 2008 to strengthen banks' capital buffers. These measures are since 2014 anchored in European legislation (Capital Requirements Directive (CRD IV) and Capital Requirements Regulations (CRR);

CRD IV

The Capital Requirements Directive (CRD IV) has been published in the Official Journal of the European Union. This publication is a milestone in the development of the supervisory framework after years of discussions, negotiations and preparations. At the same time this publication is merely one step in a continuing process of amending the supervisory framework. Significant changes to national law, supervisory policy and institutions behavior and ultimately an increased soundness of the financial system are expected to be the consequences of the CRD IV. More can be found on the ECB website here;

Standardized approaches

Basic principle of Basel 4 is that banks will make more use of standardized approaches for calculating the amount of capital and the operation of internal - own - risk models will be limited;

Capital floor of 72,5%

An important new core measure is a capital floor of 72.5%, although banks may use an internal risk model under Basel 4 to determine the necessary buffers, but that buffer may never be lower than 72.5% of the Basel 4 standardized approach.That standard model is part of Basel IV and is a lot more conservative than the models of the banks themselves. "In the crisis we saw that some parties were using internal models in an undesirable way to reduce the need for capital," said Mario Draghi. of the European Central Bank when presenting the Basel 4 agreement. That percentage of 72.5% has been the subject of considerable debate for years. After all, the higher that percentage, the higher the capital buffers must be. Dutch banks suffered relatively little loss on the mortgage portfolio during the crisis, mainly due to the high payment morality among Dutch people. The internal models have ensured that Dutch - and many other Northern European - banks have maintained relatively low capital buffers;

Capital buffers

That percentage of 72.5% has been the subject of considerable debate for years. After all, the higher that percentage, the higher the capital buffers must be. Dutch banks suffered relatively little loss on the mortgage portfolio during the crisis, mainly due to the high payment morality among Dutch people. The internal models have ensured that Dutch - and many other Northern European - banks have maintained relatively low capital buffers;

Basel 4 impact many European banks

Many European banks will have Basel 4 impact, especially Northwestern European banks, including Dutch banks. They often work with internal models and also have relatively many low-risk mortgages on the balance sheets. Starting in 2022, Dutch banks will have to maintain additional capital because the mitigating impact of the internal models will be limited due to the fact that the Dutch Central Bank decided certain Basel 4 regulations come into force from January 1st onwards. This regulation is called Regeling Risicoweging hypothecaire leningen 2022 and can be found here. DNB legitimates the new regulation as follows: De minimum vloer neemt toe naarmate de LTV-ratio’s van de onderliggende leningen hoger zijn. Hierdoor moet meer kapitaal worden aangehouden voor risicovollere hypothecaire leningen portefeuilles. Juist de hoge LTV-ratio’s van nieuwe hypothecaire leningen vormen immers een belangrijke bron van systeemrisico;

The Output floor

The output floor is one of the central elements of the Basel III reform. As the name suggests, it is a measure that sets a lower limit (“floor”) on the capital requirements (“output”) that banks calculate when using their internal models. The main aim of the output floor is to address model risk, which in this specific case is the risk that a bank's internal model incorrectly estimates the bank's capital requirements. The main concern is that internal models might underestimate the amount of capital needed by banks. Studies conducted at EU and international level showed that capital requirements calculated by internal models can vary quite significantly, even for the same risk exposure. Some of this variability cannot be explained by the characteristics of the exposures. The output floor aims to reduce this unwarranted variability and therefore to increase the comparability of capital ratios of banks using internal models.

Single or parallel stack?

Banks and their supervisors have diverging views on how to implement the output floor: banks argue for a “parallel stack” approach, while supervisors argue for a “single stack” approach. What is the difference between those two approaches? Each bank is subject to several types of capital requirements: minimum capital requirements (socalled Pillar 1), additional capital requirements imposed by the bank's supervisors (so-called Pillar 2) for risks not covered or not sufficiently covered by minimum capital requirements, and capital buffer requirements. The total capital requirement of a bank is simply the sum of all these requirements. The consequences of breaching each of the individual requirements are different. For example, breaching a minimum requirement can lead to the bank's license being withdrawn, whereas breaching a buffer leads to limitations on dividend and bonus payments. It is important how each of these capital requirements is positioned compared to the others. Therefore, the prudential rules set out the order in which the different requirements “stack” on top of each other, hence the name “capital stack”. Under the “single stack” approach for risk-based capital requirements, there would be one capital stack with all the requirements in the stack expressed in terms of the risk-weighted assets. They would be calculated in accordance with the additional step explained above. In contrast, the “parallel stack” approach would create a new stack standing alongside (“parallel” to) the existing one. Under this approach, like in the case of the existing single stack approach, the capital requirements in the parallel stack would be calculated using the risk-weighted assets calculated in accordance with the procedure outlined above. However, unlike in the case of the single stack approach, the parallel stack would not contain all necessary requirements. For example, this approach could exclude the Pillar 2 requirement and the systemic risk buffer requirement, which are important aspects of the B4 framework. With the banking package of October 2021, the European Commission clearly chose for the single stack approach.

The Transitional period

EU banks will have enough time for implementation. The final set of Basel III standards were agreed at international level by BCBS in December 2017. In response to the COVID-19 crisis, the Basel Committee decided in March 2020 to postpone the implementation deadline by one year to 1 January 2023, followed by a five-year phasing-in period of certain elements of the reform. The Commission proposes to give banks and supervisors additional time to properly implement the reform in their processes, systems and practices, and start applying the new rules from 1 January 2025. The extended implementation period will allow banks to focus on managing financial risks stemming from the COVID-19 crisis and on financing the recovery, and give them enough time to adjust before the reform reaches its full effect. Please note that the stricter capital requirements already became partly in effect for Dutch banks from the 1st of January 2022 onward due to Regeling Risicoweging hypothecaire leningen 2022 (which can be found here.).

1. Basel IV requires larger buffers

Basel IV proposes changes in the calculations of the credit, market and operational risks. This will increase risk-weighted assets (RWA) by 17.5%. This is mainly due to our mortgage portfolio. It currently consumes little capital by applying our internal model. After Basel IV, we have to hold much more capital for the exact same risk.

2. Decrease in mortgage amount

You can’t compare mortgages with each other. Mortgages with a high loan-to-value ratio carries more weight in risk and therefore higher costs within the Basel IV framework. The maximum loan-to-value ratio is now 100%. In practice, such mortgages will become too expensive for many people and private equity will therefore become increasingly important for home buyers. In doing so, Basel IV is actually forcing a reduction in the maximum mortgage amount to be financed, which has long been a fervent wish from DNB and AFM. With regard to these two parties, the maximum is legally reduced to 90% of the home value. Politics in The Hague have not yet dared to do so, because it will be even more difficult for starters to buy a house.

3. Increase minimum capital requirements

Dutch banks will face significantly higher minimum capital requirements as a result of the Basel IV standards. In some cases these higher requirements are already met through banks holding capital well in excess of current minimum requirements, but some banks will need to take important decisions on whether to improve their capital ratios through issuing new capital, retained earnings, or a reduction in risk weighted assets, during a period post Corona when return on equity is likely to remain low.

4. Threat of capital shortages

Many European banks will face significant capital shortfalls under the Basel IV reforms. According to analysis of Mckinsey, if banks do nothing to mitigate Basel IV impact, these rules will require about €120 billion in additional capital, while reducing the banking sector’s return on equity by 0.6 percentage points. This is a game changer for the European banking industry.

5. Impact of the regulations

With the newly revised output floor, the European Banking Authority (EBA) has estimated that the impact of the regulations will cause RWAs to increase by 28 percent on average, equivalent to a total capital shortfall of €135 billion for European banks. Banks will have to manage the additional capital requirements that this incurs—likely either by increasing pricing or by stepping away from certain businesses or products.

SA or IRB?

The capital adequacy ratio (CAR) of a bank is equal to the ratio of total capital and total risk-weighted assets (RWA). Total capital is defined as Tier 1 plus Tier 2 capital. Tier 1 capital is the core capital of a bank, which includes equity capital and disclosed reserves. Tier 2 capital consists of supplementary capital, such as subordinated debt, and is used to absorb losses in a case or a bankruptcy.

Banks apply the Standardized approach for the calculation of the risk weight for mortgages unless they meet the minimum conditions for the application of the Internal Ratings-based approach (IRB). The IRB approach relies on a bank's own assessment of its counterparties and exposures to calculate capital requirements for credit risk. Such an approach has two primary objectives:

- Risk sensitivity - Capital requirements based on internal estimates are more sensitive to the credit risk in the bank's portfolio of assets;

- Incentive compatibility - Banks must adopt better risk management techniques to control the credit risk in their portfolio to minimize regulatory capital.

- Categorize their exposures into various asset classes as defined by Basel 3;

- Estimate the risk parameters—probability of default (PD), loss given default (LGD), exposure at default (EAD), maturity (M)—that are inputs to risk-weight functions designed for each asset class to arrive at the total risk weighted assets (RWA)

First method:

Standardized approach (SA)

Banks can choose between two broad methodologies for calculating their risk-based capital requirements for credit risk. The first is the standardized approach (SA). Here you can find the current and future Basel rules for the calculation of the RWA for credit risk.

The standardized approach assigns standardized risk weights to exposures as described in the Basel guidance. Risk weighted assets are calculated as the product of the standardized risk weights and the exposure amount. Exposures should be risk-weighted net or specific provisions (including partial write-offs).

The current Basel 3 rule for the SA of mortgages

In applying the 35% weight, the supervisory authorities should satisfy themselves, according to their national arrangements for the provision of housing finance, that this concessionary weight is applied restrictively for residential purposes and in accordance with strict prudential criteria, such as the existence of substantial margin of additional security over the amount of the loan based on strict valuation rules. Supervisors should increase the standard risk weight where they judge the criteria are not met.

National supervisory authorities should evaluate whether the risk weights are considered too low based on the default experience for these types of exposures in their jurisdictions. Supervisors, therefore, may require banks to increase these risk weights as appropriate.

Image: © Armando Babani/ANP

Image: © Armando Babani/ANP

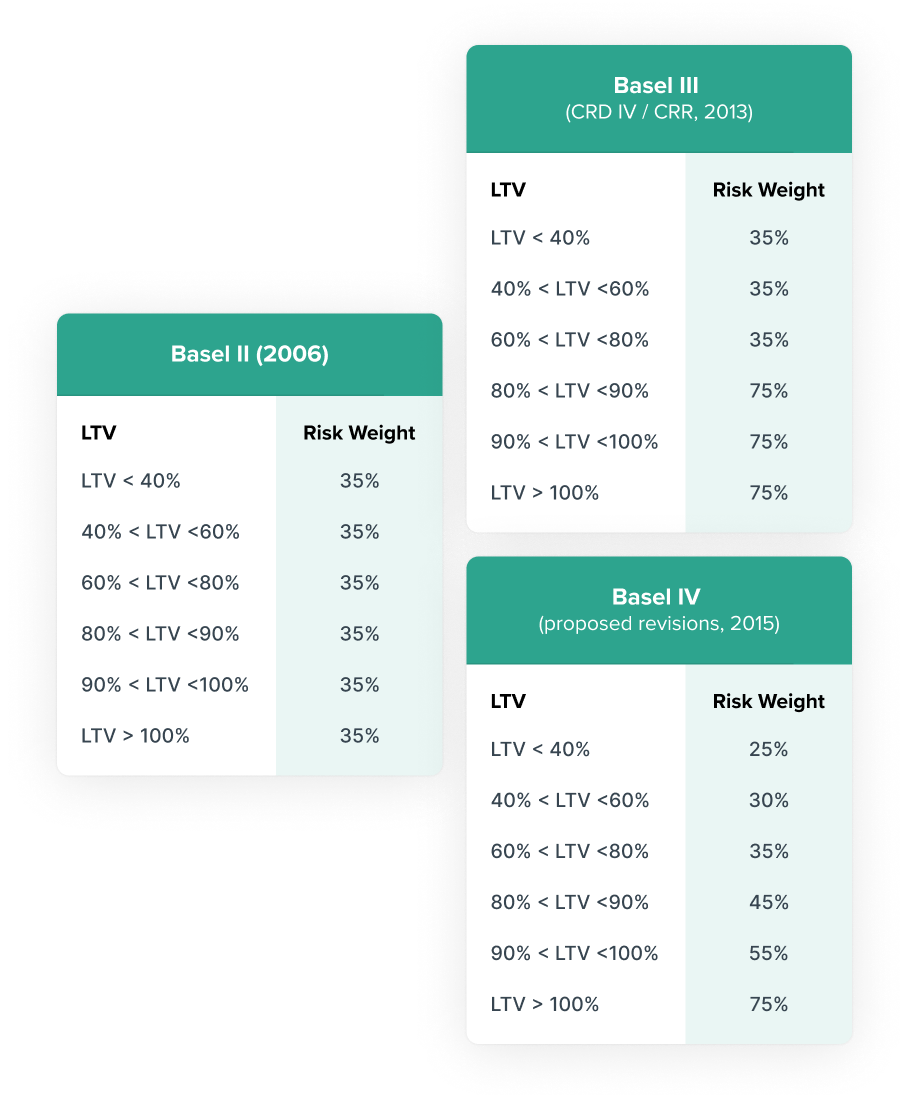

Risk weights under Basel 2 and 3

For the part of the mortgage loan exceeding the 80% LTV, the risk weight amounts to 75%. See the table below.

Example:

Bank A applies the SA and the CAR is 14%

How much capital is required for the following mortgages:

-

€ 300,000 LTV = 60%

Answer:

RWA = 35% x € 300,000 = € 105,000 -

Required capital = 14% x € 105,000 = € 14,700 -

€ 300,000 LTV = 81%

Answer:

RWA = 75% x € 300,000

Required capital = 14 % x € 225,000 = € 31,500

The RWA under SA will be further refined in Basel 4.

Method two:

internal ratings based approach (IRB)

As an alternative to the SA banks may apply the internal ratings based (IRB) approach for credit risk:

Subject to certain minimum conditions and disclosure requirements, banks that have received supervisory approval to use the IRB approach may rely on their own internal estimates of risk components in determining the capital requirement for a given exposure. The risk components include measures of probability of default (PD), loss given default (LGD), exposure at default (EAD), and effective maturity (M). In some cases, banks may be required to use a supervisory value as opposed to an internal estimate for one or more of the risk components.

Method two: internal ratings based approach (IRB)

There are three separate risk-weight functions for retail exposures. Risk weights for retail exposures are based on separate assessments of PD and LGD as inputs to the risk-weight functions.

In all cases the IRB method leads to lower RWAs than the SA. Otherwise it would not make sense using it. Since the implementation of Basel 2, banks could use an IRB approach by leveraging their internal understanding of risk measurement. This discretion has seen a rise to a common complaint that risk weights are not comparable across banks, and that some banks have been too aggressive in using models to drive down risk weights. Under Basel 4 these issues are addressed by restricting what is accepted in the IRB approach, by applying a floor (72.5%) to the extent to which risk weights can be driven down by the use of internal models, and by making the Standardized Approach more risk sensitive.

IRB: the calculation

We cannot exactly calculate the required capital according to the IRB method in the examples above. It depends on the specific bank and the loads of historical data which will be applied. However, we can be sure that the amount of capital - accounted according the current regulations - is lower than the SA outcome.

Just for the purists who like to check themselves the calculation, here it is:

Go in depth.

The original package of measures and requirements has been worked out by the Basel Committee, the international group of supervisors of the financial sector.

Basel IV and Covid-19

DNB measures taken with regard to Covid-19

- Reduction of buffer requirements for the three large banks DNB is reducing the buffers for the three large banks ING, Rabobank and ABN Amro. This creates space that the banks can use to support lending to the Dutch economy. In time, this reduction in the buffer requirements will be compensated by a gradual increase in the countercyclical capital buffer (CCyB). As a result, the total buffer requirements for these banks will eventually return to the current level;

- Postpone stricter mortgage requirements In October 2019, DNB announced a measure whereby banks should hold more capital for their mortgage loan portfolios. This measure is intended to increase the resilience of banks in the light of the increased systemic risk related to the Dutch housing market. The intended entry into force of this measure was September 2020. DNB has decided to postpone the entry into force of the measure for the time being. The measure would lead to an increase in the capital requirements for the banking sector of more than EUR 3 billion in total. This amount is released due to the postponement and can also be used to support lending. Later this year, DNB will take a decision on when the measure can still take effect. It is logical that this will be earlier than the start of the gradual build-up of the CCyB.

DNB published On 15 October 2019 measures to hold more capital against mortgage loan portfolios. The measure is a precursor to Basel4. Basically, it means that a lower limit is imposed for the risk weighting of mortgages. This increases the RWA for mortgage portfolios and thus also the capital to be held. As said, this measure is now being postponed.